Today's topic of conversation is margin rates, that is, the rate your broker charges you on a margin loan. The margin rate can have a profound impact on an investor's overall return and may even be the make-or-break factor in determining whether a given trading strategy will be profitable.

| To illustrate, let's consider the following example: say we have a investment strategy designed to produce average annualized returns of 5%. While 5% may sound meager to some investors, imagine that our strategy is a highly risk controlled one that hedges out most of the risk of overall market fluctuations (this could be a long/short portfolio for example). Therefore, leveraging the strategy up to 4 to 1 is both feasible and prudent. So, without margin (i.e. using leverage) the portfolio produces 5% annualized returns, but at a leverage ratio of 4 to 1, the porftfolio produces returns of 20%. Sounds great, no? |  Margin Rates across various on-line brokers. |

Alas, the story is never so simple. The missing piece here is that we need to deduct the cost of the margin loan from the portfolio's return. So, if our margin rate is say, 6%, then we will end up incurring a negative 1% loss for any leverage we take on (since it costs us 6% to make a return of 5%). Obviously, the cost of the margin loan negates the profitability of the trading strategy.

Now this is where it becomes interesting. The most indelible shift during the past 15 years in the brokerage industry has been the emergence of discount brokers, with their constant drive towards lower costs. Generally speaking, the effect this has had on commission structures has been to drive the entire industry towards similar commissions, as well as greater transparency on commission charges. While different discount brokers have different commission schedules, they are all within a competitive range.

Now this is where it becomes interesting. The most indelible shift during the past 15 years in the brokerage industry has been the emergence of discount brokers, with their constant drive towards lower costs. Generally speaking, the effect this has had on commission structures has been to drive the entire industry towards similar commissions, as well as greater transparency on commission charges. While different discount brokers have different commission schedules, they are all within a competitive range.

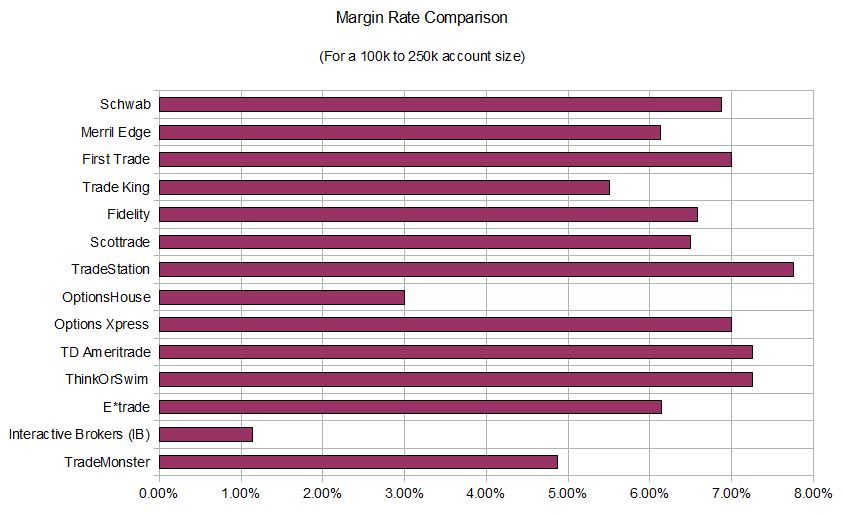

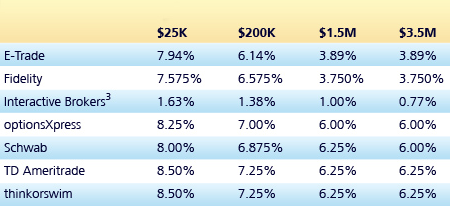

What's surprising is that the same cannot be said about margin rates. There is a huge range of margin rates across different discount brokers as is illustrated in exhibit 1 below.

Exhibit 1. Margin rates as of May 1, 2012. Source: Interactive Active Brokers website.

Exhibit 1 isn't comprehensive by any stretch of the imagination, however, it does illustrate the point. Going back to our trading strategy described earlier, only Interactive Brokers, ETrade and Fidelity charges a margin rate that would make our strategy profitable. Moreover, the strategy with Etrade and Fidelity only becomes profitable if we have an account net equity value of 1.5 million or more.

What's the lesson here? Choose your broker wisely. The margin rate can be just as important (if not more important) than commission rates, execution, technology, or service.

What's the lesson here? Choose your broker wisely. The margin rate can be just as important (if not more important) than commission rates, execution, technology, or service.

RSS Feed

RSS Feed