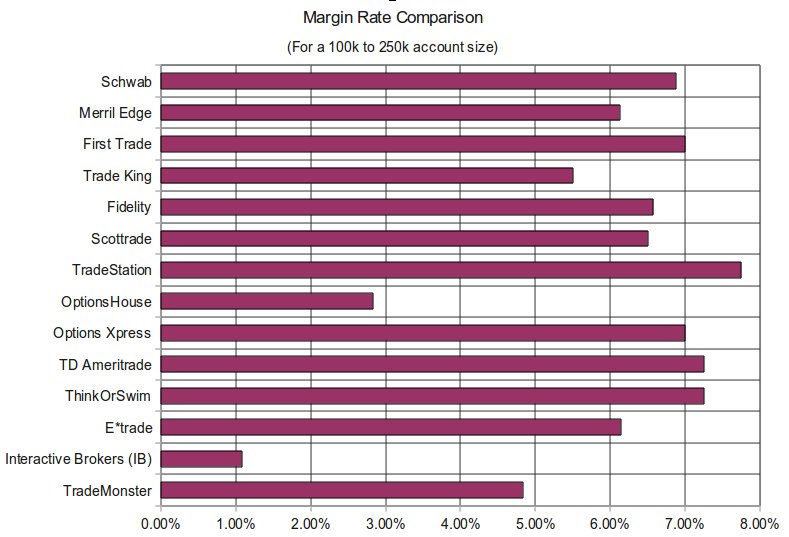

I just finished updating my comparison of broker margin rates. IB still offers (by far) the lowest margin rates, followed by OptionsHouse and TradeMonster.

After a several years of compiling this data on a regular basis, it still surprises me just how large a disparity there is between different online brokers. Brokers such as TradeStation, TD Ameritrade and ThinkOrSwim charge margin rates that are several multiples higher than other brokers.

The lesson to be learned here is that it's worthwhile to shop around for a broker with a good mix of reasonable margin rates, low commissions, good execution and other factors that make a broker attractive.

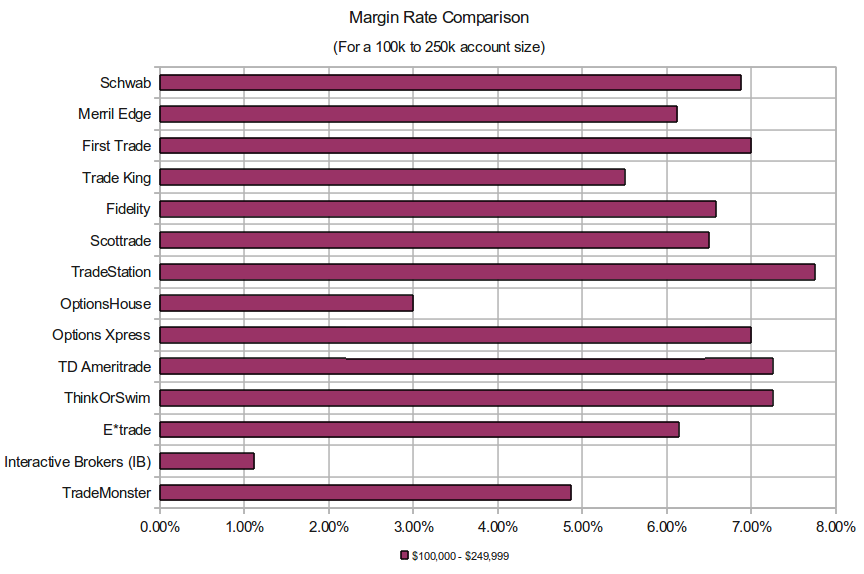

After a several years of compiling this data on a regular basis, it still surprises me just how large a disparity there is between different online brokers. Brokers such as TradeStation, TD Ameritrade and ThinkOrSwim charge margin rates that are several multiples higher than other brokers.

The lesson to be learned here is that it's worthwhile to shop around for a broker with a good mix of reasonable margin rates, low commissions, good execution and other factors that make a broker attractive.

RSS Feed

RSS Feed