I've spent a lot of time talking about the margin rates offered by various on-line brokers and the impact it can have on a trading strategy. Unfortunately, I have yet to find a decent comparison of margin rates across various brokers. While a handful of sites compile this data they are almost always lacking in some critical way (updated infrequently or incomplete in their list of brokers).

So, I've created a new page on The Margin Investor site with an updated comparison of broker margin rates.

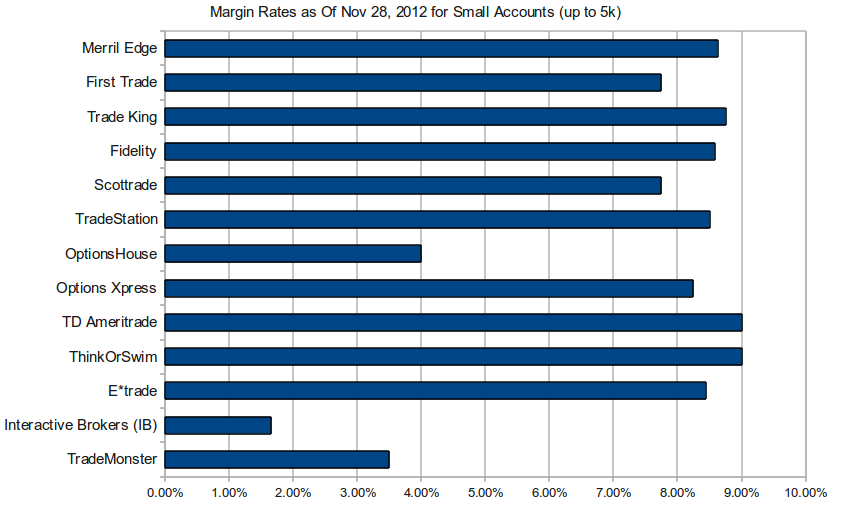

The chart below illustrates margin rates for a small brokerage account. It continues to surprise me just how how much variability there is between different brokers.

See here for the full list.

So, I've created a new page on The Margin Investor site with an updated comparison of broker margin rates.

The chart below illustrates margin rates for a small brokerage account. It continues to surprise me just how how much variability there is between different brokers.

See here for the full list.

RSS Feed

RSS Feed