One of the questions most frequently posed by readers of The Margin Investor is whether (and how) Portfolio Margin can be used to build portfolios on the higher cash flow yielding side; undoubtedly a germane question given the combination of robust yields on dividend paying stocks/corporate bonds, coupled with exceedingly low margin rates.

An attractive approach to constructing a yield focused portfolio is through the judicious use of a high yield corporate bond ETF. A good example of this is iShares iBoxx HY Corp Bond ETF (ticker: HYG) which currently yields around 7%. This ETF tracks the performance of a diversified basket of US corporate non-investment grade bonds. Without further ado, let's walk through an example.

An attractive approach to constructing a yield focused portfolio is through the judicious use of a high yield corporate bond ETF. A good example of this is iShares iBoxx HY Corp Bond ETF (ticker: HYG) which currently yields around 7%. This ETF tracks the performance of a diversified basket of US corporate non-investment grade bonds. Without further ado, let's walk through an example.

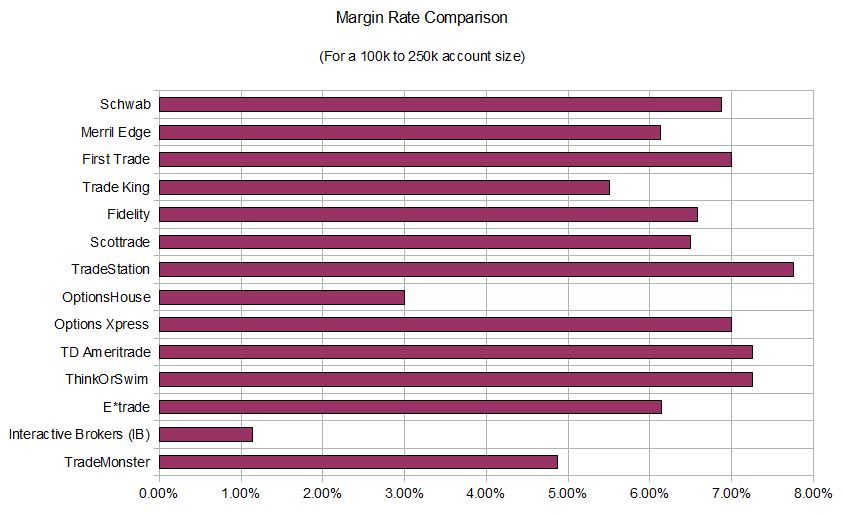

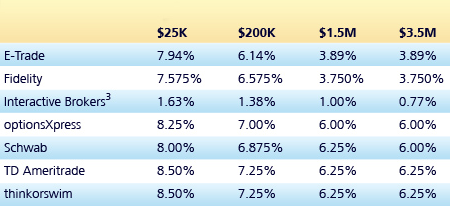

Fist, assume we have an Interactive Brokers account such that our margin borrowing rate is 1.7%. Under Portfolio Margin, we can leverage this up to 3 to 1 (or more depending on risk appetite) in order to obtain a gross yield of 21%. To calculate the net yield, we minus the IB margin rate cost of 3.4% (1.7% * 2), which results in a net yield of 17.6%. By using leverage, we've converted a 7% yielding portfolio to a portfolio yielding 17.6%. That's 1.47% per month flowing directly into our brokerage account.

| By using leverage, we've converted a 7% yielding portfolio to a portfolio yielding 17.6%. That's 1.47% per month flowing directly into our brokerage account. |

HYG from June 6, 2010 to June 6, 2012.

What's the catch? Well, there's always a catch. The added yield comes with additional risk. Specifically, the fund is exposed to the following two core risk factors:

So, the bottom line here is this strategy is only for you if you believe the Fed is committed to continuing its policy of low interest rates and provided you don't expect to see any problems in credit markets. We'll leave it to the reader to decide if this is a prudent strategy. Regardless, this portfolio will pay you handsomely while you wait.

In the next article, we will examine the risk of this portfolio in more detail.

- Interest Rates - when interest rates go up the fund will lose value. According to my calculations the fund's effective duration to medium term rates is around 7. This means that if the medium term gov interest rates move up around 50 bps (i.e. half a percent), the HYG ETF will go down roughly 3.5%. On our leveraged portfolio, this would be a 10.5% loss.

- Credit Spreads - as corporate credit spreads increase, the HYG ETF will lose value. Of course, the converse is also true. This is essentially a bet that the economy will continue to improve (or at least not deteriorate).

So, the bottom line here is this strategy is only for you if you believe the Fed is committed to continuing its policy of low interest rates and provided you don't expect to see any problems in credit markets. We'll leave it to the reader to decide if this is a prudent strategy. Regardless, this portfolio will pay you handsomely while you wait.

In the next article, we will examine the risk of this portfolio in more detail.

RSS Feed

RSS Feed