In the previous post we examined the use of bond ETFs such as the iShares iBoxx HY Corp Bond ETF (ticker: HYG) to create a portfolio with an annualized dividend yield of over 17% net of margin borrowing costs. This involved taking on a leveraged position in HYG. The amount of leverage discussed was 3-to-1 and, as a result, a Portfolio Margin account was recommended.

We concluded the previous post by warning about the risks involved with this type of highly leveraged fixed income ETF position. In today's post, we look at the risk profile of this strategy from a scientific standpoint. The tables below are taken from our risk system which evaluates portfolio risk using a multi-factor risk model.

We concluded the previous post by warning about the risks involved with this type of highly leveraged fixed income ETF position. In today's post, we look at the risk profile of this strategy from a scientific standpoint. The tables below are taken from our risk system which evaluates portfolio risk using a multi-factor risk model.

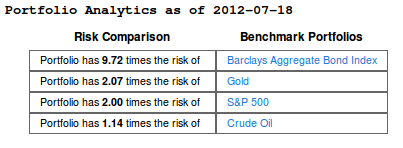

Table 1. Risk Comparison for the 3 times leveraged HYG portfolio.

Table 1 above shows the risk of the leveraged HYG portfolio in comparison to the risk of other well known assets. As can be discerned from table 1, the 3 times leveraged HYG portfolio is twice as risky (where risk is measured in terms of volatility of future returns) as the S&P 500 portfolio (ticker: SPY) but has only a little more risk than a portfolio consisting of a Crude Oil ETF (ticker: USO).

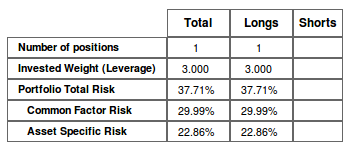

| Table 2 shows the Portfolio Total Risk and breaks it down into Common Factor Risk and Asset Specific Risk. Common factors are forces that influence a large number of stocks (think of things like yield curve movements and changes in credit spreads). Asset specific forces emanate from risk tied only to this particular ETF (e.g. characteristics of the specific bonds in the ETF's portfolio). |  Table 2. Portfolio Risk for the 3 times leveraged HYG portfolio. |

On row three of Table 2 we can see that the Portfolio Total Risk is 37.71%. This means that the expected annualized standard deviation of the portfolio's return is 37.71%.

Table 3. Risk Decomposition for the 3 times leveraged HYG portfolio.

We can also investigate the sources of this risk. Table 3 above displays the Common Factors the Portfolio is exposed to (column 1), the exposure level of the portfolio to these common factors (column 2), and the decomposition of the risk across the common factors (last column). As the table indicates, the majority of the portfolio's risk emanates from the exposure of this fund to the High Yield Credit Spread factor. This is evident by looking at the column on the far right of table 3, which lists this factor's contribution to the overall portfolio risk. The numbers in the last column are additive (i.e. sum to the the Portfolio's Total Risk). Interestingly, the portfolio's exposure to changes in the yield curve actually decrease the portfolio's overall risk since interest rates and credit spreads are negatively correlated.

So, what can we glean from the above analysis? There are three key takeaways:

- The 3 times leveraged HYG portfolio gives you a net dividend yield of over 17%, but comes with the risk of a 2 times leveraged SPY portfolio.

- By far and away the biggest source of risk is High Yield Credit Spreads. Therefore, it's imperative that you believe the economic picture is improving. A blow out of credit spreads could slam this portfolio hard.

- Our analysis points to ways to hedge out a big chunk of the credit spread risk, while keeping most of the dividend yield. We will explore this in a future article.

RSS Feed

RSS Feed